22 / 36

22 / 36

The week of 18 August– 24 August 2016

Volume 28 Number 01

Stocks selected under this section are meant for medium and/or long-term investments. When stocks are recommended under this section, it does not mean that its price will take 1 or 2 years to move. If the price moves too

fast,

i

Capital® may recommend a sell. Or if it is still attractive after holding for a while and its price has gone up, we may still recommend holding or even buying more. Or if it declines,

i

Capital® quotes Warren Buffett who

was supposed to have said this : “If you aren’t prepared to see your stocks go down 50%, you shouldn’t own them. Be prepared for declines – and arrange your financial affairs such that you won’t have to sell out”.

B.1. UMW Oil & Gas Corporation (UMWOG, 5243)

This week,

i

Capital

provides an update on UMW

Oil & Gas Corporation Bhd

(UMW OG) which was listed

on the KLSE in Nov 2013.

The last time

i

Capital did

the write up on the company

was almost a year ago. How

have things changed for this

one-time favourite of the

investor community ?

UMW OG is mainly

involved in providing

drilling rigs for the oil and

gas industry. In general,

there are 3 classes of

rigs; namely, jack up rigs,

semi-submersible rigs and

drillships. The difference

lies in the depth of the

waters where the well is to

be drilled. Jack up rigs can

drill in shallow waters with

depths of up to 450 feet (ft)

while semi-submersibles and

drillships can drill up to 9,000

ft and beyond respectively.

UMW OG owns 7 jack up

rigs and 1 semi-submersible.

The jack up is also the

most common in the oil and

gas industry and the cost

averages around US$200

mln each (approximately

RM800 mln).

Singapore-based Keppel

KFELS (a subsidiary of

Keppel Corporation) and

Sembcorp Marine are among

the major builders of jack up

rigs and semi-submersibles

in the world. However, in the

recent years, the Chinese

yards have come up in terms

of quality besides their lower

price and more attractive

financing arrangements

with customers. They

have done so by recruiting

the Singaporean project

managers to their yards

and from there acquiring

the required skills. A surge

in orders before oil price

plunged and then cut back

in investment spending by

the global oil majors led to

an oversupply of jack up rigs

that is currently plaguing the

market.

Updates

In Sep 2015,

SapuraKencana Energy

Peninsula Malaysia

Inc., SapuraKencana

Energy Sarawak Inc. and

SapuraKencana Energy

Sabah Inc (collectively as

SKPetro), awarded the

company a contract for

the provision of its NAGA

8 drilling capabilities. The

work is for up to 18 wells

with an extension option for

3 additional wells. So far

6 wells have been drilled.

The programme runs until

Nov 2017. NAGA 7 is also

on contract with Petronas

Carigali S/B (PCSB) to drill

7 wells with an extension

option of 1 plus 1 well

starting from Oct 2015.

PCSB is the exploration and

production arm of Petroliam

Nasional Bhd, the national

oil company of Malaysia. The

estimated duration of 1 well

is 1 month. This contract is

nearing its end.

In May 2016, the

company received a letter

of award from PCSB for its

NAGA 6 to participate in

its drilling programme. The

contract which will start in

4Q 2016, is for 2 years with

a 1-year option to extend.

While this is expected to

contribute positively, drilling

rigs are charged based

on their daily charter rate

(DCR). The higher the

number of days the rigs is

used, the higher the number

of days UMW OG can charge

the customer the DCR and

vice versa. If the customer

does not use the rig, UMW

OG is not able to charge the

DCR. With activities having

been cut drastically, the

utilisation is not expected

to be high over the contract

period. In addition, due to

the oversupply of jack up

rigs as mentioned earlier,

the DCR has also fallen

drastically.

Table 1

shows its

respective rigs and

contracts.

Unlike Perisai Petroleum

Bhd which has been

delaying the delivery of its

second and third jack up

rigs thereby avoiding to

recognise the respective

expenses and borrowings on

its balance sheet, UMW OG

already has taken delivery

of its rigs and therefore

recorded them onto its

books. It is in an even more

desperate situation to get

contracts to justify its sunk

costs and investments. Even

though its jack up rigs are

being warm stacked, UMW

OG still needs to account for

the annual depreciation and

interest cost over the life of

30 years and the term of the

loan respectively.

Already having seen its

total borrowings ballooned

from RM860 mln in

FY2013 to RM3.6 bln as

of 1Q FY2016 and in dire

need for cash, its parent

company, conglomerate

Principal activities

Provides offshore services

to oil & gas exploration and

production industry.

Major shareholder/s

UMW Holdings Bhd, Skim

Amanah Saham Bumiputera.

Latest paid-up

2.162 bln shares of RM0.50 each

Market capitalisation

RM2.119 bln @ RM0.98

2016 P/E Ratio:

NA@ RM0.98

Sources: UMW OG, Capital Dynamics

1st quarter RM mln

31/03/16 31/03/15

Sales

87.68 312.5

Pretax profit

-68.42 42.46

Net profit

-65.08 32.15

Finance cost

26.03 11.80

Depreciation

68.36 48.98

Cash and cash

equivalent

887.9 973.8

UMWOG is

mainly involved

in

providing drilling rigs for the oil and

gas industry.

Financial highlights (RM mln) – 31 December

2011

2012

2013

2014

2015

Sales

550.3

724.3

737.8

1,015

839.9

Pre-tax profit

102.1

74.38

206.9

284.2

-348.4

Net profit

78.31

61.83

190.6

252.0

-369.3

Adjusted net profit

80.33

63.70

172.0

218.7

-353.4

Depreciation

49.63

57.10

89.34

133.1

246.1

Finance cost

31.46

40.15

23.74

26.09

64.06

Current assets

401.7

519.5

1,626

1,718

1,557

Current liabilities

835.0

978.4

498.4

1,533

2,555

Fixed assets

1,258

1,477

2,247

4,022

6,081

Total assets

1,709

2,065

3,891

5,756

7,646

Total debt

799.8

798.5

859.6

2,255

4,004

Return on equity (%)

156.3

37.86

70.48

7.719

NA

Source: UMW Oil & Gas Corporation

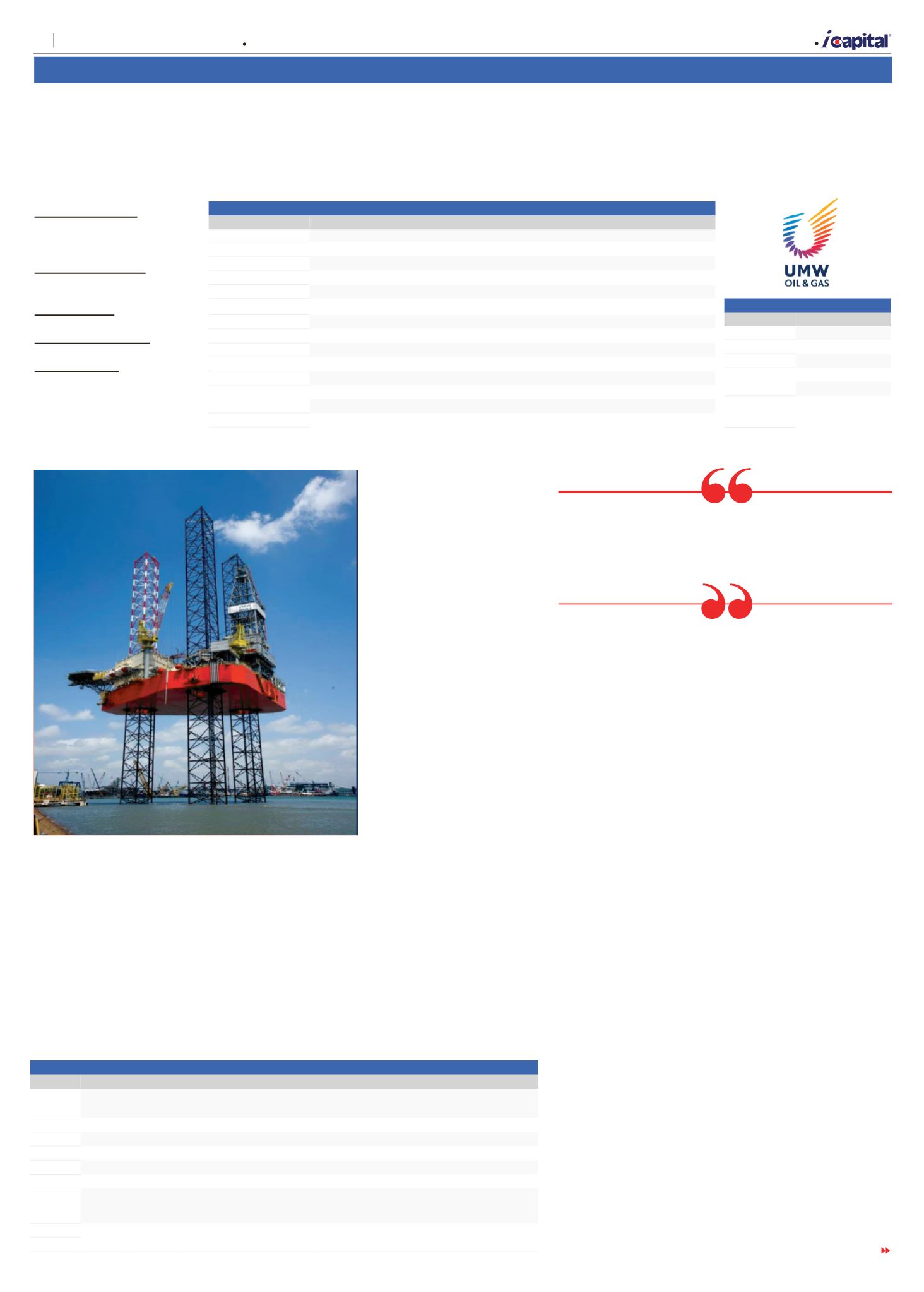

Naga 4 .

Table 1 UMW OG’s Rigs

Rig name Rig type Delivery

Builder

Current client and contract

NAGA 1 Semi-

sub

1974 Mitsubishi Heavy Industries On hire with PCSB from Nov 2010 to Aug 2018

NAGA 2 Jack up

2009

PT Drydocks

Warm stacked

NAGA 3 Jack up

2010

PT Drydocks

Warm stacked

NAGA 4 Jack up Feb 2013

Keppel FELS

Warm stacked

NAGA 5 Jack up May 2014

Keppel FELS

Warm stacked

NAGA 6 Jack up Sep 2014 Tianjin Haiheng Shipbuiliding

With PCSB for 2 years + 1 year. To start in 4Q 2016

NAGA 7 Jack up Dec 2014 Tianjin Haiheng Shipbuiliding Contract with PCSB nearing its end. No subse-

quent contract.

NAGA 8 Jack up Sep 2015

Keppel FELS

With SKPetro for 18 wells + 3 wells ending Nov 2017.

Source: UMW OG

TURN TO PAGE 23

B

| Stock Selections

22

Capital Dynamics Sdn Bhd