10 / 24

10 / 24

growth have also been well

telegraphed and intended.

Otherwise, how to rebalance

China’s economy ? We all

knew these for years; the

Western media knew these

for years.

What is surprising is that

the stable

economic

growth in

China in

the last few

years has

instead been

interpreted and

reported in

the media and

analyst reports

as China’s

economy

crashing

and heading

for a major

crisis. As an

independent

and objective

investment

adviser, Capital

Dynamics

sees this type

of reporting

and analysis

as wrong,

worrying and

dangerous.

i

Capital needs

to protect

and project

the truth. As

the plunge in

oil price and

China’s stock

market still

dominate the headlines and

the reports, one needs to

look at the other unreported

developments. For example,

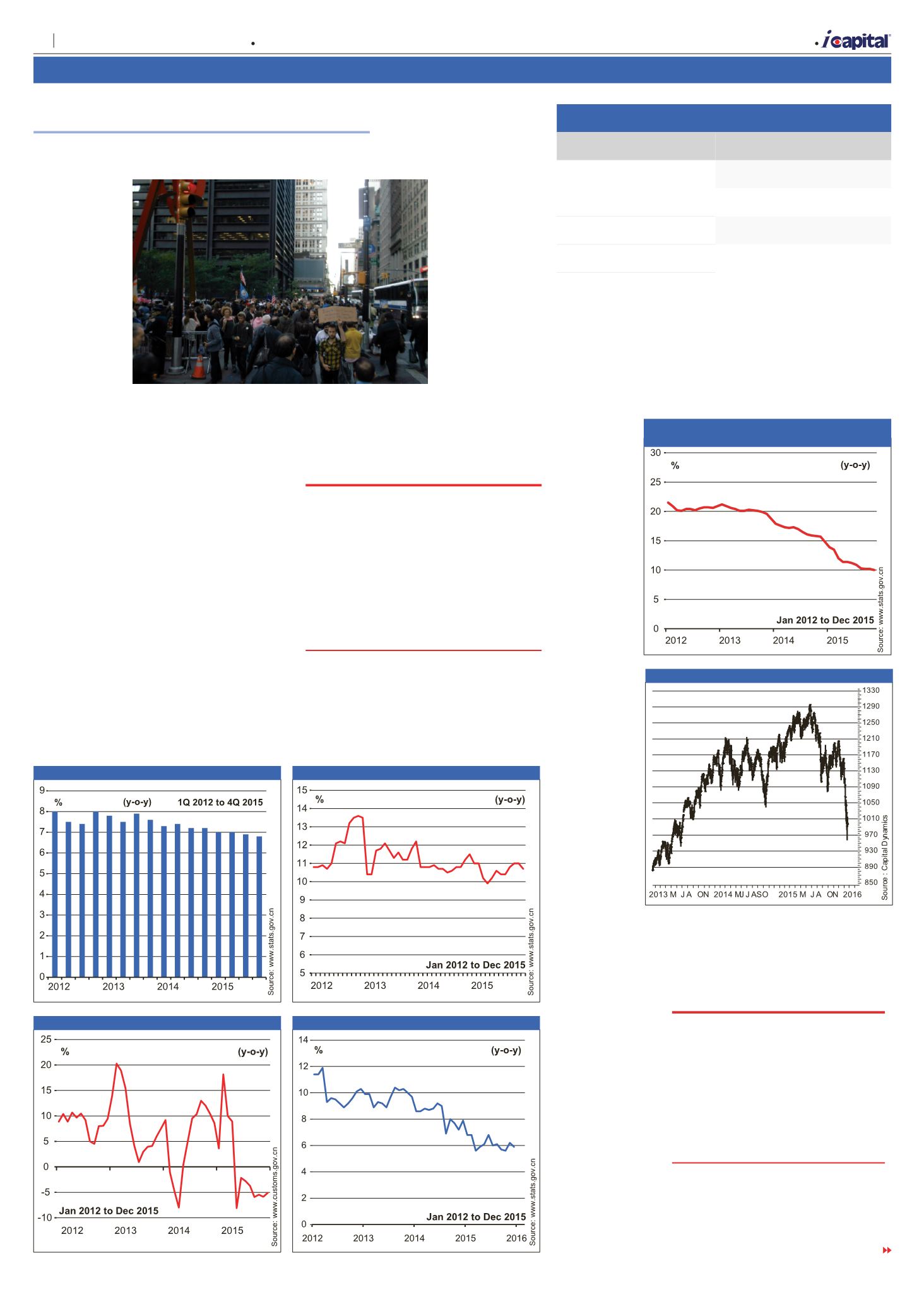

the Russell 2000 Index is

already in a bear market (see

figure 6

).

The Russell

2000 Index is a

small-cap stock

market index of

the bottom 2,000

stocks in the Russell

3000 Index. The

S&P 500 index is

used primarily for

large capitalisation

stocks. The Russell

2000 Index is the most

widely quoted measure of

the overall performance of

the small-cap to mid-cap

shares. American small-caps

are an excellent way to

China have been

weak as far back

as 2012-2013,

thanks partly to

a super strong

Renminbi, which

China did not

complain at all

and a weak

global economy.

Figures 1 to 3 tell

us that the latest

supposed “weak”

economic data

from China is

nothing new. We

all knew this for

years; the Western

media knew this for years. So,

why such a ruckus now ?

What have been weak are

industrial production (

figure

4

) and fixed asset investment

(

figure 5

). Both have been

climbing down steadily since

2013. Well, what do you

know ? These declines in

So far, the

media

headlines

are still mainly

dominated by

falling crude

oil price, the

supposed

troubled China

economy and

crashing stock

market. The

plunge in crude

oil price is

certainly worthy

of very close

attention. For

one, substantial

movements in

oil price always have major

global implications. Two,

except for a very few people

like Tan Teng Boo, very few

foresaw, as early as he did,

oil price crashing to below

US$30. So, it is not surprising

for the plunging oil price to

capture the headlines. The

same cannot be said for the

current slowdown in China’s

economy though.

Why ? For one thing, the

economic slowdown in China

has been going on for years.

It is the most telegraphed,

the most intended, and the

most well planned economic

slowdown in the history of

mankind. The leaders from

China have been saying the

same message for years.

Figure 1

shows China’s GDP

growth since 2012. It was

already at the 7-8% range.

What is the big deal about

6.9% now ? Why make such

a big fuss ? You

all knew it was

coming, and it

came. The same

can be said for

China’s retail

sales.

Figure

2

is adjusted

for inflation and

what do you

know ? Real

retail sales have

been growing

in the low teens

for years. Ha, exports, you

say exports have been falling

and China desperately needs

to weaken the Renminbi to

be competitive. Again,

figure

3

tells us that exports from

avoid the adverse effects

of international tensions as

well as to avoid the negative

impact of a strong US$ on

corporate earnings. A much

smaller proportion of revenues

from American small-cap

companies are generated

abroad relative to the

large-cap companies, which

make up the S&P 500. If

China and the falling oil price

are adversely affecting the

global stock markets, why is

it that the Russell 2000 Index

is performing worse than the

S&P 500 ? Why is it that the

Russell 2000 Index is already

“If China and the falling oil

price are adversely affecting

the global stock markets, why

is it that the Russell 2000 Index

is performing worse than the

S&P 500 ? Why is it that the

Russell 2000 Index is already in

a bear market ?”

“For one thing, the economic

slowdown in China has been

going on for years. It is the most

telegraphed, the most intended,

and the most well planned

economic slowdown in the history

of mankind. The leaders from

China have been saying the same

message for years”

A.4. KLSE Conclusion

PROJECTING THE TRUTH

Source: Capital Dynamics

Occupy Wall Street in 2011. Will it

repeat soon ?

TURN TO PAGE 11

KLSE Composite Index : Market Valuation

21 Jan 2016 14 Jan 2016 15 Jan 2015

PE Ratio

17.56 17.89 16.69

Div Yield

3.15

3.09

3.38

Price/Bk Value

1.75

1.79

2.11

FBM KLCI

1,600.92 1,633.44 1,745.00

Source: Bursa Malaysia, Capital Dynamics

Figure 5 Cumulative Fixed Asset Investment

(Excluding rural households)

Figure 6 Russell 2000 Index

Figure 4 Industrial Production

Figure 2 Real Retail Sales

Figure 3 China’s Exports (3-months moving average in US$)

Figure 1 China’s Real GDP

A

| Market Opinion

10

Capital Dynamics Sdn Bhd

The week of 21 January – 27 January 2016

Volume 27 Number 21